Get Premium

Dark mode theme is available exclusively for premium users. Learn more about the benefits of subscribing.

No fees, cancel anytime.

Dark Mode Ad-Free Browsing Unlimited Content

Dark Mode Ad-Free Browsing Unlimited Content

Ad-Free Browsing Unlimited Content Dark Mode

Ad-Free Browsing Unlimited Content Dark Mode

Join 1.2 million Panda readers who get the best art, memes, and fun stories every week!

Businesses put a lot of effort into figuring out the right prices for their products. Set it too low, and you leave money on the table. Make it too high, and you can say goodbye to sales that could have made your year.

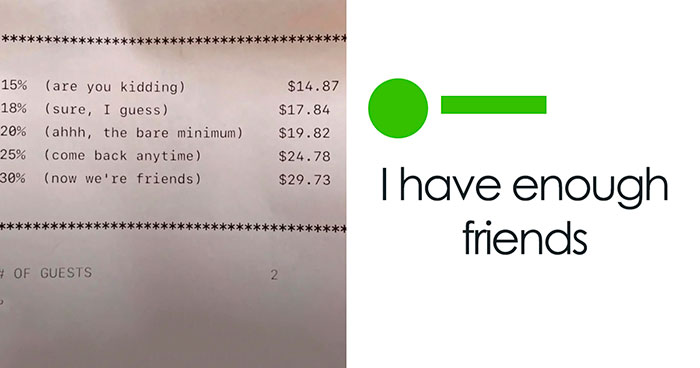

Finding the ideal number means choosing a strategy that’s appropriate for that particular situation. And Imgur user ShlomoGenchin thought it would be interesting to explore some of the most common options.

But what’s really awesome, after they did all the homework, ShlomoGenchin decided to summarize everything in simple visualizations and post the images online where everyone could see them.

Image credits: ShlomoGenchin

Image credits: ShlomoGenchin

Image credits: ShlomoGenchin

Image credits: ShlomoGenchin

Image credits: ShlomoGenchin

Image credits: ShlomoGenchin

Image credits: ShlomoGenchin

Image credits: ShlomoGenchin

Image credits: ShlomoGenchin

Image credits: ShlomoGenchin

Image credits: ShlomoGenchin

Image credits: ShlomoGenchin

Image credits: ShlomoGenchin

The phenomenon that identical products are perceived differently due to differences in price is called the “marketing placebo effect” and just as with medications, it has an effect solely due to ascribed properties: “Quality has its price!”

To illustrate the effect pricing has on consumers, ShlomoGenchin concluded their post with an excerpt from a 2017 study, conducted by scientists from the INSEAD Business School and the University of Bonn.

The researchers invited 30 participants (of which 15 were women and 15 were men, with an average age of around 30 years) and offered them some wine.

The wine tasting took place lying down in an MRI scanner, allowing brain activity to be recorded while participants were sipping. But each time, the price of the wine was shown first. Only then around a milliliter of the respective wine was administrated to the test person via a tube in their mouths. The participants were then asked to rate with a push of a button on a nine-point scale how good the wine tasted to them.

Their mouths were then rinsed with a neutral liquid and the next identical wine sample was given for tasting.

“As expected, the subjects stated that the wine with the higher price tasted better than an apparently cheaper one,” Professor Hilke Plassmann from the INSEAD Business School reported.

“However, it was not important whether the participants also had to pay for the wine or whether they were given it for free.”

“How much the customer is willing to pay for the product has very little to do with the seller’s cost and has very much to do with how much they value the product or service they’re buying,” Eric Dolansky, Associate Professor of Marketing at Brock University in St. Catharines, Ontario, told BDC, the bank for Canadian entrepreneurs.

According to Dolansky, pricing is one decision that shouldn’t be driven by accounting.

The customer needs to find that the price falls within their range of what’s acceptable, and a company’s ability to price is constrained by its costs.

To choose the right price within the customer’s acceptable range, businesses must consider the following factors:

Different pricing strategies can and do co-exist as a product evolves through its lifecycle in the market. Companies need an overall price strategy (e.g., cost-based or value-based), they need to determine generally how high or low the price will be (skimming and penetration pricing), and they need to respond to competitors (competition-based pricing).

For example, someone may want to initially price their product using a value-based approach, then switch to a skimming strategy and conclude with penetration pricing.

Pricing is one of the most important and visible aspects of market strategy, which also includes promotion, placement (or distribution), and people (a formula, known as the classic Four Ps of marketing).

The price you offer, Dolansky said, must be consistent with “how you would like to be seen among your competitors, and consistent with your promotional messages, your packaging, and types of stores that your product is in.”

Suppose your product is premium olive oil. It needs to have a premium price that reflects the refined packaging, distribution in better grocery stores, and upscale promotional messages.

However, at the end of the day, all pricing strategies are double-edged swords. What attracts some customers will repulse others. Nobody can sell all things to all people.

538Kviews

Share on FacebookThis is why you learn algebra and percentages, so you can work out the cost per unit or cost per volume to work out which is actually the best deal.

Ever see the Penn & Teller show, "Bullsh!t"? They had an episode where they made a fancy restaurant with a "water sommelier", but they just used the same water (from a garden hose out back) and just used fancy bottles and poetic descriptions and charged high prices, and everyone was like "Ooh this water is so much better!". It was hilarious 😂

I love when this kind of exposé is made. I watched a different show that used brownies that were stale/a few days old to emphasize how presentation matters to taste. One was wrapped in plastic and picked up at the counter by the till, the other was in a glass case, served on a glass plate with a fork and a light dusting of icing sugar. They were from the same original pan/batch. Guess which one repeatedly "tasted better" even before being eaten.

Load More Replies...My local supermarket has just pulled a psychological trick. They have removed most of the small trolleys so that people are forced to use the larger ones. In return they feel stupid or feel it is a waste of a journey for only putting a few items in a big trolley so buy more things.

Lol, I hate it when places do that, because I end up just doing w/o a cart, and buying what I can carry w/me. Good for my budget, bad for my ability not to drop things

Load More Replies...This is why you learn algebra and percentages, so you can work out the cost per unit or cost per volume to work out which is actually the best deal.

Ever see the Penn & Teller show, "Bullsh!t"? They had an episode where they made a fancy restaurant with a "water sommelier", but they just used the same water (from a garden hose out back) and just used fancy bottles and poetic descriptions and charged high prices, and everyone was like "Ooh this water is so much better!". It was hilarious 😂

I love when this kind of exposé is made. I watched a different show that used brownies that were stale/a few days old to emphasize how presentation matters to taste. One was wrapped in plastic and picked up at the counter by the till, the other was in a glass case, served on a glass plate with a fork and a light dusting of icing sugar. They were from the same original pan/batch. Guess which one repeatedly "tasted better" even before being eaten.

Load More Replies...My local supermarket has just pulled a psychological trick. They have removed most of the small trolleys so that people are forced to use the larger ones. In return they feel stupid or feel it is a waste of a journey for only putting a few items in a big trolley so buy more things.

Lol, I hate it when places do that, because I end up just doing w/o a cart, and buying what I can carry w/me. Good for my budget, bad for my ability not to drop things

Load More Replies...

No fees, cancel anytime

No fees, cancel anytime

114

74