Bank Sends This Person An Ambiguous “Super Predatory” Letter About An Unpaid Debt From 2 Decades Ago, Luckily They Read It Carefully

Usually, getting mail is great. You might open up your mailbox to find a postcard from a long-forgotten friend or an invitation to support a local cause you care about deeply. However, right at the back of your mailbox you might find a bill or… a debt collection letter.

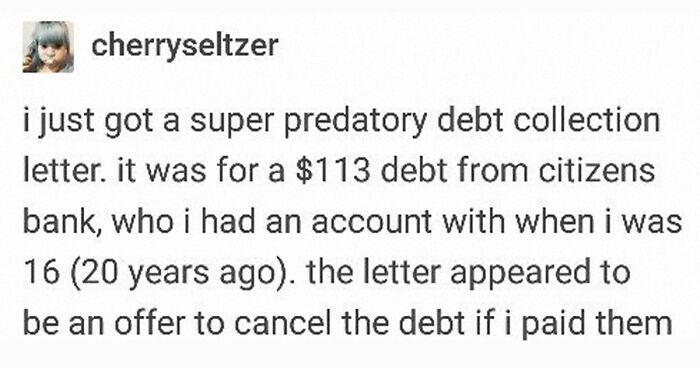

A Tumblr user, who goes by the name of Cherryseltzer, shared their story about a weird and “super predatory” debt collection letter they got. And it got their alarm bells ringing. The letter’s full of ambiguity and it’s bound to make anyone want to complain about getting something like this.

Scroll down, have a read, and let us know what you think, dear Pandas. Have you gotten anything like this yourselves? What’s the best thing to do in a situation like this? Share your thoughts in the comment section.

Someone shared their negative experience with a bank letter and it’s a warning about how you should read everything very carefully

Image credits: Daniel Arauz (not the actual photo)

Image credits: cherryseltzer

Image credits: feetlips

Paying off your debts and honoring your agreements is important. However, letters about a minuscule debt from over 2 decades ago that make you wish you had a lawyer on retainer don’t exactly help improve a company’s reputation.

And what makes my head spin the most is that actually making any repayments toward the debt (even though you don’t have to) would make it possible for the bank to sue you for the full amount. I might be old-fashioned, but aren’t things that are legal supposed to be connected to the spirit of justice (just a tiny bit)?

Cherryseltzer’s story got nearly 122k notes on Tumblr. The story made a resurgence in popularity on Imgur recently, too, with nearly 5.9k upvotes. Naturally, the people who read the story online were shocked and suggested that everyone read all letters and contracts very carefully. And one commenter took the cake when they summed up the entire situation in a single sentence: “Pay us so we can sue you.”

Debt collection laws vary country to country and state to state, so you’ll need to do some research and read up on what is and isn’t allowed if you get any similar letters. And if you’re confused, there are always people and organizations who offer pro bono advice about legal matters. Just make sure to always, always, always read the fine print.

Here’s what people said when they read about what happened

Fun story - I once had a crown put in by a dentist who screwed up my insurance paperwork so I ended up having to pay for the whole massive bill out of pocket. It wiped out my meager savings, but I paid it completely. A couple months later, I start getting harassing and threatening phone calls at home and at work from a debt collection agency acting on behalf of the dentist. The debt in question? One cent. Let me repeat that. ONE. CENT. The icing on this particular crud cake was that when I went directly to the dentist to have it out with them, it turns out HE owed ME.

Should have turned it over to a debt collection agency so they could harass him. Unbelievable. I'm sure that was the last time you ever used that dentist.

Load More Replies...The comment inside the article by ErikMare, "Am I the only person that believes in paying your debts?": I don't think this applies. This is a tiny debt from almost a generation ago to Citizens Bank, likely from a banking error (say $6 for being 24h in unauthorised overdraft); paying $6--$10 I would agree is "paying your debts". HOWEVER, Citizens Bank has recently sold this for a similar amount (say $2--$5) to this predatory company; so CB has effectively made its money back (you being 24h in red doesn't actually cost them anything; it's all paperwork). Paying this $23 to this vulturine third party however will oblige to paying the rest of the $113 PLUS COSTS --- non of which is "debts"... So NO paying this is NOT PAYING DEBTS --- you don't OWE them anything. They are professional gamblers in essence, they "bought" the debt and are gambling with it (if 1 in 10 is scared enough for their credit rating then they're making money). Banks are really an essential service, these aren't.

I always pay my debts with the caveat that they must be my legitimate debts to pay. I once took my kids to a clinic for their annual maintenance exams, which are fully covered by our insurance. The clinic billed the exams as sports physicals, which insurance does not cover, and sent me a bill for just under $400. I pleaded with them for months to bill the insurance properly, but they refused and ended up sending the debt to collections. I fought collections for several years until they finally just stopped sending me a bill. I had a huge sigh of relief when seven years passed without any further mention of it and I knew I was free of it. It's been about 12 years now and my daughter got dehydrated one night and our options were that clinic for urgent care or the ER which would cost much more. They said they wouldn't treat my daughter unless I paid over $900 "towards the unpaid bill". I have no idea what total they have ballooned it to, but I never owed it in the first place.

Load More Replies...You'd have to be real careful... not only could you wind up owing the $113... but can you imagine if those bastards tried to hook on 20 some years worth of interest?

Maybe get the title right. The bank did not send it, jefferson capital sent it which is a collection agency. The bank has long ago written it off.

They hadn't written it off, they sold the debt to a collection agency. Perhaps they only got $25 out of it, but they didn't write it off. The remainder of the debt will be booked as loss and the taxpayer will pay for that.

Load More Replies...When I was a teenager (96-98) my grandmother had a Mervyn's card (I miss Mervyn's) she added me as an authorized user but back then it wasn't a card holder it just meant I could use the card in store. The deal with my grandma was that whatever I spent I had to pay when the bill came in and then every year for school she'd pitch in 100 for school clothes I didn't have to pay back. YEARS later my grandma passes (2006) about three years later I get a call from a collection agency saying I owed a bill for a couple of thousand dollars. I asked for what they said Mervyn's. I told them I never had an account. They asked if I knew a Carolyn I said yes my grandmother. They said "well you were an authorized user so you are responsible" I audibly laughed in this ladies face. I said oh yea? When was this? She said "approximately 1997" I said "Lady I was born in 1981 you do the math. That puts me at 16 years old and not of age to enter a legal binding contract. Never heard back lol.

Laughs in European and thinks about authorities that are eager to come down on fraudsters like 10 ton of bricks.

Yes Zombie debt is real and perfectly legal in the eyes of the law. If you start to repay an old debt you have contractually acknowledged you still owe the debt and are willing to pay it. This form of debt collection should be blocked by UDAAP practices but it's not. However, I urge all Americans to read the new UDAAP updates as more stringent restrictions against 3rd party debt collectors will be in place soon. A 3rd part debt collector does not work for the company you owe the debt to.

the other time was a dentist who agreed to take payments for a bill of $275 but his aggressive office manager didn't agree to this so began an attack on my. i even contacted the dentist who confirmed the agreement but then told me his wife was the manager. after almost a month of bi weekly calls i went into the office to pay...with unrolled pennies. yes, it was petty. at first she refused to take it but i told her it was legal tender and if she didn't accept then i guess i didn't owe. then she told me to count it; told her not my job. so, i sat down, took a thermos of coffee out , some crocheting and waited for her to count every damn coin.

I got a letter from that exact company, same kind of letter. I requested an explanation of the debt through certified mail, just to have the record. They never sent me the explanation and legally can't continue to try to collect the debt until they do. So when I received more collection letters after that 30 days, I reported them to the FTC. The collection company sent me a letter about two weeks after the complaint that they were going to officially retire the debt (I can't remember the exact wording).

OK, so I LEGIT just got the same letter for a debt of 530$ from verizon on an account I never had. (Long story) anyways. Said they'd knock it down to 295$ but they'd be willing to take a payment of 147$ and also states its so old they can't sue unless I restart the debt 😂😂😂 like byeeee. JEFFERSON CAPITAL SYSTEMS LLC.

it wasn't the Bank who sent the letter - it was a Junk debt buyer ; an assignee of the bank , jefferson capital systems

I use to do collections on medical bills and I’d have to actually call people over debt less than $10, which can’t be reported to their credit bc the debt is too small. Why do hospitals actually bother with that? To make it worse I actually with a straight face had to say I’m calling you about your $3 balance. It was insane

this kind of stuff happens also on the phone. prior to retiring i got a call regarding a phone bill from over 10 yrs before that had accumulated so called interest to over $500. guy was super aggressive and threatening. he asked who my employer was and, while i normally would not give that info, this time it worked so well: officer for the district attorney. he suddenly said he would have to check with his employer to see how to take action against govt employee...and never heard back from him again.

It should be an offense even sending out demands like this for time-barred debts. If you have a law, let's apply it to it's practical extent, both ways, not just one way.

Another trick: medical services will try to balance bill you for the remainder after your insurance pays them. If they are a preferred provider, they cannot legally do so.

Most of these comments make me sad. Why is everyone trying to get away with something/not do the right thing? If I found out I owed money, I would be embarrassed that I had not paid and I would pay it, no matter the statute of limitations. I would call the company, find out if this were a legitimate debt, and if it were, I would apologize and pay.

You think it's going to stop there? They will backdate the interest and compound it so that from $100, you will be owing thousands!

Load More Replies...You don't even need a lawyer, as long as this person ignores the letter the bank can't do anything. Especially since the so called "debt" is only $113...a lawyer would cost so much more.

Load More Replies...In this case, just read carefully... Legal aid completely overrun by demand.

Load More Replies...Fun story - I once had a crown put in by a dentist who screwed up my insurance paperwork so I ended up having to pay for the whole massive bill out of pocket. It wiped out my meager savings, but I paid it completely. A couple months later, I start getting harassing and threatening phone calls at home and at work from a debt collection agency acting on behalf of the dentist. The debt in question? One cent. Let me repeat that. ONE. CENT. The icing on this particular crud cake was that when I went directly to the dentist to have it out with them, it turns out HE owed ME.

Should have turned it over to a debt collection agency so they could harass him. Unbelievable. I'm sure that was the last time you ever used that dentist.

Load More Replies...The comment inside the article by ErikMare, "Am I the only person that believes in paying your debts?": I don't think this applies. This is a tiny debt from almost a generation ago to Citizens Bank, likely from a banking error (say $6 for being 24h in unauthorised overdraft); paying $6--$10 I would agree is "paying your debts". HOWEVER, Citizens Bank has recently sold this for a similar amount (say $2--$5) to this predatory company; so CB has effectively made its money back (you being 24h in red doesn't actually cost them anything; it's all paperwork). Paying this $23 to this vulturine third party however will oblige to paying the rest of the $113 PLUS COSTS --- non of which is "debts"... So NO paying this is NOT PAYING DEBTS --- you don't OWE them anything. They are professional gamblers in essence, they "bought" the debt and are gambling with it (if 1 in 10 is scared enough for their credit rating then they're making money). Banks are really an essential service, these aren't.

I always pay my debts with the caveat that they must be my legitimate debts to pay. I once took my kids to a clinic for their annual maintenance exams, which are fully covered by our insurance. The clinic billed the exams as sports physicals, which insurance does not cover, and sent me a bill for just under $400. I pleaded with them for months to bill the insurance properly, but they refused and ended up sending the debt to collections. I fought collections for several years until they finally just stopped sending me a bill. I had a huge sigh of relief when seven years passed without any further mention of it and I knew I was free of it. It's been about 12 years now and my daughter got dehydrated one night and our options were that clinic for urgent care or the ER which would cost much more. They said they wouldn't treat my daughter unless I paid over $900 "towards the unpaid bill". I have no idea what total they have ballooned it to, but I never owed it in the first place.

Load More Replies...You'd have to be real careful... not only could you wind up owing the $113... but can you imagine if those bastards tried to hook on 20 some years worth of interest?

Maybe get the title right. The bank did not send it, jefferson capital sent it which is a collection agency. The bank has long ago written it off.

They hadn't written it off, they sold the debt to a collection agency. Perhaps they only got $25 out of it, but they didn't write it off. The remainder of the debt will be booked as loss and the taxpayer will pay for that.

Load More Replies...When I was a teenager (96-98) my grandmother had a Mervyn's card (I miss Mervyn's) she added me as an authorized user but back then it wasn't a card holder it just meant I could use the card in store. The deal with my grandma was that whatever I spent I had to pay when the bill came in and then every year for school she'd pitch in 100 for school clothes I didn't have to pay back. YEARS later my grandma passes (2006) about three years later I get a call from a collection agency saying I owed a bill for a couple of thousand dollars. I asked for what they said Mervyn's. I told them I never had an account. They asked if I knew a Carolyn I said yes my grandmother. They said "well you were an authorized user so you are responsible" I audibly laughed in this ladies face. I said oh yea? When was this? She said "approximately 1997" I said "Lady I was born in 1981 you do the math. That puts me at 16 years old and not of age to enter a legal binding contract. Never heard back lol.

Laughs in European and thinks about authorities that are eager to come down on fraudsters like 10 ton of bricks.

Yes Zombie debt is real and perfectly legal in the eyes of the law. If you start to repay an old debt you have contractually acknowledged you still owe the debt and are willing to pay it. This form of debt collection should be blocked by UDAAP practices but it's not. However, I urge all Americans to read the new UDAAP updates as more stringent restrictions against 3rd party debt collectors will be in place soon. A 3rd part debt collector does not work for the company you owe the debt to.

the other time was a dentist who agreed to take payments for a bill of $275 but his aggressive office manager didn't agree to this so began an attack on my. i even contacted the dentist who confirmed the agreement but then told me his wife was the manager. after almost a month of bi weekly calls i went into the office to pay...with unrolled pennies. yes, it was petty. at first she refused to take it but i told her it was legal tender and if she didn't accept then i guess i didn't owe. then she told me to count it; told her not my job. so, i sat down, took a thermos of coffee out , some crocheting and waited for her to count every damn coin.

I got a letter from that exact company, same kind of letter. I requested an explanation of the debt through certified mail, just to have the record. They never sent me the explanation and legally can't continue to try to collect the debt until they do. So when I received more collection letters after that 30 days, I reported them to the FTC. The collection company sent me a letter about two weeks after the complaint that they were going to officially retire the debt (I can't remember the exact wording).

OK, so I LEGIT just got the same letter for a debt of 530$ from verizon on an account I never had. (Long story) anyways. Said they'd knock it down to 295$ but they'd be willing to take a payment of 147$ and also states its so old they can't sue unless I restart the debt 😂😂😂 like byeeee. JEFFERSON CAPITAL SYSTEMS LLC.

it wasn't the Bank who sent the letter - it was a Junk debt buyer ; an assignee of the bank , jefferson capital systems

I use to do collections on medical bills and I’d have to actually call people over debt less than $10, which can’t be reported to their credit bc the debt is too small. Why do hospitals actually bother with that? To make it worse I actually with a straight face had to say I’m calling you about your $3 balance. It was insane

this kind of stuff happens also on the phone. prior to retiring i got a call regarding a phone bill from over 10 yrs before that had accumulated so called interest to over $500. guy was super aggressive and threatening. he asked who my employer was and, while i normally would not give that info, this time it worked so well: officer for the district attorney. he suddenly said he would have to check with his employer to see how to take action against govt employee...and never heard back from him again.

It should be an offense even sending out demands like this for time-barred debts. If you have a law, let's apply it to it's practical extent, both ways, not just one way.

Another trick: medical services will try to balance bill you for the remainder after your insurance pays them. If they are a preferred provider, they cannot legally do so.

Most of these comments make me sad. Why is everyone trying to get away with something/not do the right thing? If I found out I owed money, I would be embarrassed that I had not paid and I would pay it, no matter the statute of limitations. I would call the company, find out if this were a legitimate debt, and if it were, I would apologize and pay.

You think it's going to stop there? They will backdate the interest and compound it so that from $100, you will be owing thousands!

Load More Replies...You don't even need a lawyer, as long as this person ignores the letter the bank can't do anything. Especially since the so called "debt" is only $113...a lawyer would cost so much more.

Load More Replies...In this case, just read carefully... Legal aid completely overrun by demand.

Load More Replies...

152

45