Husband Comes Up With The Idea Of Pretending To Be His Wife On A Call With The Bank To Be Able To Sort Out Her Account Issue

Banks are a pretty stressful environment to be in as they have so many rules and are strict about following them, the contracts are confusing and your life kind of depends on them in certain situations.

This couple experienced it firsthand when they wanted to open a bank account and there was some kind of miscommunication on the bank’s end, but they weren’t very helpful at sorting it out. The bank also started avoiding their calls by bringing up rules that didn’t really matter previously, so the husband had to become a bit more creative and finally got what they both wanted.

More info: Reddit

A man shared the time he had to pretend to be his wife because the bank was trying to take her money when she didn’t do anything wrong

Image credits: frankieleon (not the actual image)

It happened 15 years ago when the OP’s wife wanted to open a checking account after having one closed because of insufficient funds

Image credits: u/ThrowOhWaitNo

The Original Poster (OP), or ThrowOhWaitNo as he is known on Reddit, told a story that took place 15 years ago when he and his wife were young and were not very smart with their finances as they’d had their checks rejected because they didn’t have enough money in their accounts, so they had them closed.

They were offered a way of fixing their checking account history by a large bank that the OP calls Fells Wargo in the story. It was called a rehab account, which meant they would pay an additional $10/month fee and it would have restricted funds, but if they followed the rules, they could have a regular checking account after a year.

Image credits: u/ThrowOhWaitNo

She believed she would have to open a rehab account, which was more restrictive, but she would be upgraded to a regular one after a year

Image credits: u/ThrowOhWaitNo

The husband used the opportunity to fix his checking history, but the wife lived without a checking account for a few years and decided she wanted to apply again. So the OP took her to the Fells Wargo bank to get her started with the rehab account, but the manager told them she could have the regular one right away.

It surprised the couple and they were trying to make sure if there wasn’t a mistake, but the manager reassured them everything was fine and took an initial cash deposit of $500 and the only thing left was to wait for the ATM card to come in the mail.

The manager at the bank assured the woman she could open up a regular one right away, so she agreed

Image credits: u/ThrowOhWaitNo

After a week, when she had to call the bank to activate her ATM card, she found out the account was closed because of her bad checking history

Image credits: u/ThrowOhWaitNo

After a week, the ATM card came and to activate it, the wife had to call the bank. Instead of having the card activated, the bank consultant told her that the account was closed altogether because they had determined that her checking history was too bad to have a regular account and they couldn’t change it over the phone, so she would need to come back to the bank.

This was quite frustrating as the couple had specifically asked for the rehab account and the manager was the one who convinced them to open a regular one, but they had now turned around and closed it.

On top of not informing her about it, the bank also refused to cover those checks, even though there was money in that closed bank account

Image credits: u/ThrowOhWaitNo

Image credits: Sascha Kohlman (not the actual image)

The wife didn’t have experience dealing with banks, so the OP asked her to put the consultant on speaker to ask some questions. Firstly, he wanted to know if the bank would pay the outstanding checks and refund the rest.

The bank refused to do that, even though there was enough money in the account to pay the people those checks were written for. The OP started asking more uncomfortable questions, such as why they were forced to open this account when they should have had the rehab one, and why the bank didn’t notify their clients their account was closed.

After a bit of arguing, the consultant hung up and after calling another time, they refused to talk to anyone other than the account owner

Image credits: u/ThrowOhWaitNo

The bank consultant didn’t have any answers to that and wanted to put the blame on the couple for not doing anything wrong. They were so flustered that they just straight up hung up.

The couple called back and this time, before the consultant hung up again, they said that they wouldn’t talk to anyone who was not the owner of the account, meaning the husband couldn’t talk in place of his wife or even be the mediator to help her understand what was going on.

The wife didn’t have experience talking to banks, so she wasn’t able to demand that the bank give her money back

Image credits: u/ThrowOhWaitNo

Knowing that, the OP decided to pretend to be his wife as he knew everything about the account and was determined to set the record straight

Image credits: u/ThrowOhWaitNo

The husband had a stupidly genius idea. He decided to just pretend to be his wife as he knew everything about her situation and the account and had the experience of dealing with banks, knowing they couldn’t just take the money in the account when the owner didn’t do anything wrong.

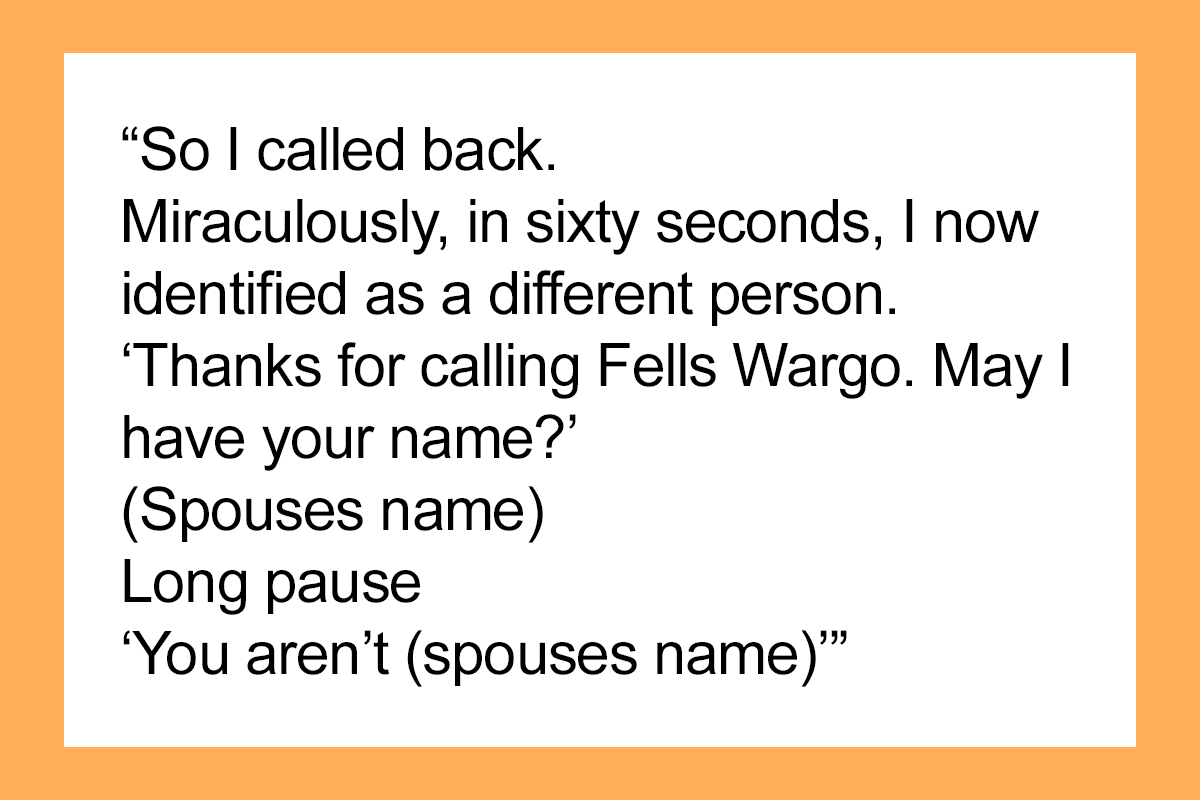

When the consultant picked up the phone and the OP introduced himself as his wife, he heard a long pause and the person on the other side was in disbelief. When the OP answered every safety question correctly, they still didn’t believe him because he clearly had a man’s voice and the name on the account was a woman’s.

Eventually he was successful because there was nothing preventing him from getting what he required

Image credits: u/ThrowOhWaitNo

Image credits: U.S. Department of Agriculture (not the actual image)

The OP quickly caught onto that and started accusing the bank of being discriminatory and closing the account just because he was a man. This conversation probably confused the consultant and made them suspicious, so the OP was referred to a manager.

The manager eventually agreed to pay the 3 checks from the funds in the account because the name on the account demanded it, but the OP felt that they still didn’t want to do it, even though there was money on the account and it was closed because of the bank’s mistake.

In response to this story, people shared their own stories of dealing with banks and their stupid rules that had no logic to them. We would like to know if you liked how the husband handled the situation and if you have any similar stories, tell us about them in the comments!

The incident is not an isolated one and people in the comments shared their own experiences of having to deal with stupid bank rules

The bank f*cked up the account creation, and were wrong to try and apply fees which resulted from that error. However, from that point on this guy is an ahole. They were 100% right that they should not be discussing the account with someone who isn't the account holder, and cannot discuss if a third party is prompting the replies the account holder is given. Discussing it as much as they did, and continuing after they knew he was impersonating the account holder is already a massive breach of regulations. Why could his partner not just talk to them as it's her account?

Yes! This pissed my off so much. I understand his frustrations not getting answers, but if you dominate a conversation when you're not on the account, and you call impersonating the account holder, I'm not doing s**t for you. I may even make it more difficult for you, especially after he threw in the discriminatory part. F**k this dude.

Load More Replies...I seriously don't get the American system of banks and cards and whatnot

It's not that hard. The banks aren't really a service for customers, it's a business to make money. They take your money and use it to make investments (turn a profit) for the bank. In return, they give you a pittance of the profit (interest). Your money just doesn't sit there, they use it for their own benefit. They loan you money and charge you more interest, than they give you for your "loan", to them! If the bank folds, you aren't even guaranteed to get ALL your money back. It's a legal pyramid, scheme. Credit unions are much better.

Load More Replies...When I went to college the school I went to had a deal with Wells Fargo. All students MUST have a Wells Fargo account, it was part of the school registration process and attached to your student ID. There were no exceptions. I moved to a different school and spent the next 5 years trying to close the account that I hadn't used a single time. The only reason it got closed was because my husband's ex was a manager at a Wells Fargo and took care of it for me.

As far as the cable one goes this is what my old employer did "we have reason to believe that a person with all of this account holders information is attempting to access this account fraudulently. Because of that positive photo ID will be required. You can go to our lobby, or we could schedule a meeting at your home if you are unable to travel"

I hate Wells Fargo so much! They are the worst bank out there. They steal your money with a smile. Im in the process of opening a different account and I can’t wait for the day I can go in there and close all my accounts. Including my partners and our joint! Mwahahahah!

I'm a banker so I'm probably going to get flayed but... there are legal reasons we can't talk to anyone other than the account holder. It's a fraud issue. It's a simple fix; talk to account holder about putting you on the account- don't get mad at me! Also, the bank isn't rubbing their hands together just waiting to give you a fee. It's automatic. And lets talk about *why* they're getting them. When your account goes into the negative, you get a fee. It's part of the agreement you agree to before opening your account. It's not the bank's fault a company went in to collect a bill or you forget how much you had in your account. You get fees at an atm because it costs money to service them. You get fees when you ask for things that you can get through other means like statements that you can access yourself online. All the bank owes you is keeping your money safe. If you want a service that isn't included with your account plan, expect a charge. It's like any other business. (1)

(2) I agree some fees, like uncollected funds fees, are stupid and 9x out of 10 if you ask (and haven't abused it), we'll reverse them for you. But spending 240 dollars at a bar the previous night and then a bill comes out and put you into the negative isn't the bank's fault. Spending all of your money at the casino then complaining to us because we're so unfair about giving you fees when you're broke is not our fault. And there's only so much we can do for you. Some things take time. You are not the only client. When asking for something it goes into a queue of other requests, all of whom think they're the most important. Banks mess up-absolutely because human error exists in all things. And in those cases the bank should make it right. In the above case, they should have made it right immediately. but people sometimes need to admit that they simply aren't paying attention to how their bills come out. It's not all the *evil* bank's doing.

Load More Replies...I had a mortgage through #Wells F-U. I sold my house and bought another through Chase Bank. Within days of selling/buying a house, Wells F-U listed my old house as a foreclosure on my credit report. This was around the time Wells F-U was all over the news and being investigated. I still had to get a lawyer, but just as quickly as that foreclosure was put on my account, it disappeared. One day it was there, the next day it was gone. It really scares me that it's so easy to F-up somebody's credit that would take years to fix.

The way the US deregulated their industries has been biting them in the a**e for decades. I understand being pro-business but never at the expense of consumers. In this case, the bank dare to pull that stunt because there isn't much repercussions. Even in the comparatively underdeveloped places I tend to do my business in, banks pulling any c**p can get a hefty fine from the central banking regulatory body.

I will only ever use a credit union. I worked for TD Canada Trust as a casual employee and then CIBC for a couple years. Even with my “employee discount” on my mortgage it was still cheaper at my credit union. I had to have an account there for my pay to go into. Right after it went in I took it out and deposited it to my credit union. My CU fees are less than 10.00 a month no matter if I go into overdraft or not. CIBC was 12.95 fees plus 25 for using overdraft. My credit union I’m always greeted by name, they always have tellers ready and every last person is helpful.

I laugh at how backwards America is with cheques. Lol use instant bank transfers here, funds arrive within seconds to any bank.

Just as a note, there's no mention of 'wife' in the post, only 'spouse'. And the spouse is specifically identified as 'they', not 'her' or 'she'. Be a better journalist. Also, it's pretty shitty how large companies can basically get away with making mistakes that cost them money, and WE have to end up paying for it. But if we make a mistake? Oh no you have to pay for that too.

My wife and I used to be WF customers, when we lived in the US (we're in the UK now). My wife was able to get British citizenship through her mother, and Irish citizenship through her maternal grandmother. My wife has US, UK, and Irish passports. At one point, the UK wanted her to send funds, in pounds sterling, to cover the cost of her citizenship application. WF kept saying they'd transfer the funds to the UK--then they'd cancel the transaction at the last minute, "because of potential fraud!" This happened at least 3x before my wife got someone on the phone to try to explain to them, again, that wanting to send money to the UK was not "fraud" on her part. My wife was on speakerphone the whole time. When the WF employee asked to speak to me, they were surprised that I was there and had been listening the whole time--apparently they thought the alleged "fraud" was my wife trying to pull a fast one on me, and/or hide money from me somehow. No matter what we said or did (part 1)

...or who we talked to, we absolutely could not convince WF that it was a legitimate transaction, and my wife really did need to send money to the UK. We ended up opening an account with USAA instead. They were ready, willing, and able to send the funds to the UK, no problem. The best part? At one point we both tried to use our current WF debit cards, and both cards were declined. Next thing we know, we both get new WF debit cards in the mail, "because we canceled your old cards as a fraud protection procedure! You should be grateful we care so much about your financial security!"

Load More Replies...The bank f*cked up the account creation, and were wrong to try and apply fees which resulted from that error. However, from that point on this guy is an ahole. They were 100% right that they should not be discussing the account with someone who isn't the account holder, and cannot discuss if a third party is prompting the replies the account holder is given. Discussing it as much as they did, and continuing after they knew he was impersonating the account holder is already a massive breach of regulations. Why could his partner not just talk to them as it's her account?

Yes! This pissed my off so much. I understand his frustrations not getting answers, but if you dominate a conversation when you're not on the account, and you call impersonating the account holder, I'm not doing s**t for you. I may even make it more difficult for you, especially after he threw in the discriminatory part. F**k this dude.

Load More Replies...I seriously don't get the American system of banks and cards and whatnot

It's not that hard. The banks aren't really a service for customers, it's a business to make money. They take your money and use it to make investments (turn a profit) for the bank. In return, they give you a pittance of the profit (interest). Your money just doesn't sit there, they use it for their own benefit. They loan you money and charge you more interest, than they give you for your "loan", to them! If the bank folds, you aren't even guaranteed to get ALL your money back. It's a legal pyramid, scheme. Credit unions are much better.

Load More Replies...When I went to college the school I went to had a deal with Wells Fargo. All students MUST have a Wells Fargo account, it was part of the school registration process and attached to your student ID. There were no exceptions. I moved to a different school and spent the next 5 years trying to close the account that I hadn't used a single time. The only reason it got closed was because my husband's ex was a manager at a Wells Fargo and took care of it for me.

As far as the cable one goes this is what my old employer did "we have reason to believe that a person with all of this account holders information is attempting to access this account fraudulently. Because of that positive photo ID will be required. You can go to our lobby, or we could schedule a meeting at your home if you are unable to travel"

I hate Wells Fargo so much! They are the worst bank out there. They steal your money with a smile. Im in the process of opening a different account and I can’t wait for the day I can go in there and close all my accounts. Including my partners and our joint! Mwahahahah!

I'm a banker so I'm probably going to get flayed but... there are legal reasons we can't talk to anyone other than the account holder. It's a fraud issue. It's a simple fix; talk to account holder about putting you on the account- don't get mad at me! Also, the bank isn't rubbing their hands together just waiting to give you a fee. It's automatic. And lets talk about *why* they're getting them. When your account goes into the negative, you get a fee. It's part of the agreement you agree to before opening your account. It's not the bank's fault a company went in to collect a bill or you forget how much you had in your account. You get fees at an atm because it costs money to service them. You get fees when you ask for things that you can get through other means like statements that you can access yourself online. All the bank owes you is keeping your money safe. If you want a service that isn't included with your account plan, expect a charge. It's like any other business. (1)

(2) I agree some fees, like uncollected funds fees, are stupid and 9x out of 10 if you ask (and haven't abused it), we'll reverse them for you. But spending 240 dollars at a bar the previous night and then a bill comes out and put you into the negative isn't the bank's fault. Spending all of your money at the casino then complaining to us because we're so unfair about giving you fees when you're broke is not our fault. And there's only so much we can do for you. Some things take time. You are not the only client. When asking for something it goes into a queue of other requests, all of whom think they're the most important. Banks mess up-absolutely because human error exists in all things. And in those cases the bank should make it right. In the above case, they should have made it right immediately. but people sometimes need to admit that they simply aren't paying attention to how their bills come out. It's not all the *evil* bank's doing.

Load More Replies...I had a mortgage through #Wells F-U. I sold my house and bought another through Chase Bank. Within days of selling/buying a house, Wells F-U listed my old house as a foreclosure on my credit report. This was around the time Wells F-U was all over the news and being investigated. I still had to get a lawyer, but just as quickly as that foreclosure was put on my account, it disappeared. One day it was there, the next day it was gone. It really scares me that it's so easy to F-up somebody's credit that would take years to fix.

The way the US deregulated their industries has been biting them in the a**e for decades. I understand being pro-business but never at the expense of consumers. In this case, the bank dare to pull that stunt because there isn't much repercussions. Even in the comparatively underdeveloped places I tend to do my business in, banks pulling any c**p can get a hefty fine from the central banking regulatory body.

I will only ever use a credit union. I worked for TD Canada Trust as a casual employee and then CIBC for a couple years. Even with my “employee discount” on my mortgage it was still cheaper at my credit union. I had to have an account there for my pay to go into. Right after it went in I took it out and deposited it to my credit union. My CU fees are less than 10.00 a month no matter if I go into overdraft or not. CIBC was 12.95 fees plus 25 for using overdraft. My credit union I’m always greeted by name, they always have tellers ready and every last person is helpful.

I laugh at how backwards America is with cheques. Lol use instant bank transfers here, funds arrive within seconds to any bank.

Just as a note, there's no mention of 'wife' in the post, only 'spouse'. And the spouse is specifically identified as 'they', not 'her' or 'she'. Be a better journalist. Also, it's pretty shitty how large companies can basically get away with making mistakes that cost them money, and WE have to end up paying for it. But if we make a mistake? Oh no you have to pay for that too.

My wife and I used to be WF customers, when we lived in the US (we're in the UK now). My wife was able to get British citizenship through her mother, and Irish citizenship through her maternal grandmother. My wife has US, UK, and Irish passports. At one point, the UK wanted her to send funds, in pounds sterling, to cover the cost of her citizenship application. WF kept saying they'd transfer the funds to the UK--then they'd cancel the transaction at the last minute, "because of potential fraud!" This happened at least 3x before my wife got someone on the phone to try to explain to them, again, that wanting to send money to the UK was not "fraud" on her part. My wife was on speakerphone the whole time. When the WF employee asked to speak to me, they were surprised that I was there and had been listening the whole time--apparently they thought the alleged "fraud" was my wife trying to pull a fast one on me, and/or hide money from me somehow. No matter what we said or did (part 1)

...or who we talked to, we absolutely could not convince WF that it was a legitimate transaction, and my wife really did need to send money to the UK. We ended up opening an account with USAA instead. They were ready, willing, and able to send the funds to the UK, no problem. The best part? At one point we both tried to use our current WF debit cards, and both cards were declined. Next thing we know, we both get new WF debit cards in the mail, "because we canceled your old cards as a fraud protection procedure! You should be grateful we care so much about your financial security!"

Load More Replies...

73

33